InsightsWhat is trade based money laundering (TBML)?

As anti-money laundering (AML) controls evolve, criminals find new ways to transform the financial proceeds of crime into legitimate funds. One of the most prevalent global money laundering strategies is to exploit the vulnerabilities of cross-border trade via trade based money laundering.

What is trade based money laundering?

Trade based money laundering (TBML) is the process of moving illegal funds through the international trade system to legitimize them. TBML practices can include the falsification of price, quantity, and quality of the imported or exported goods.

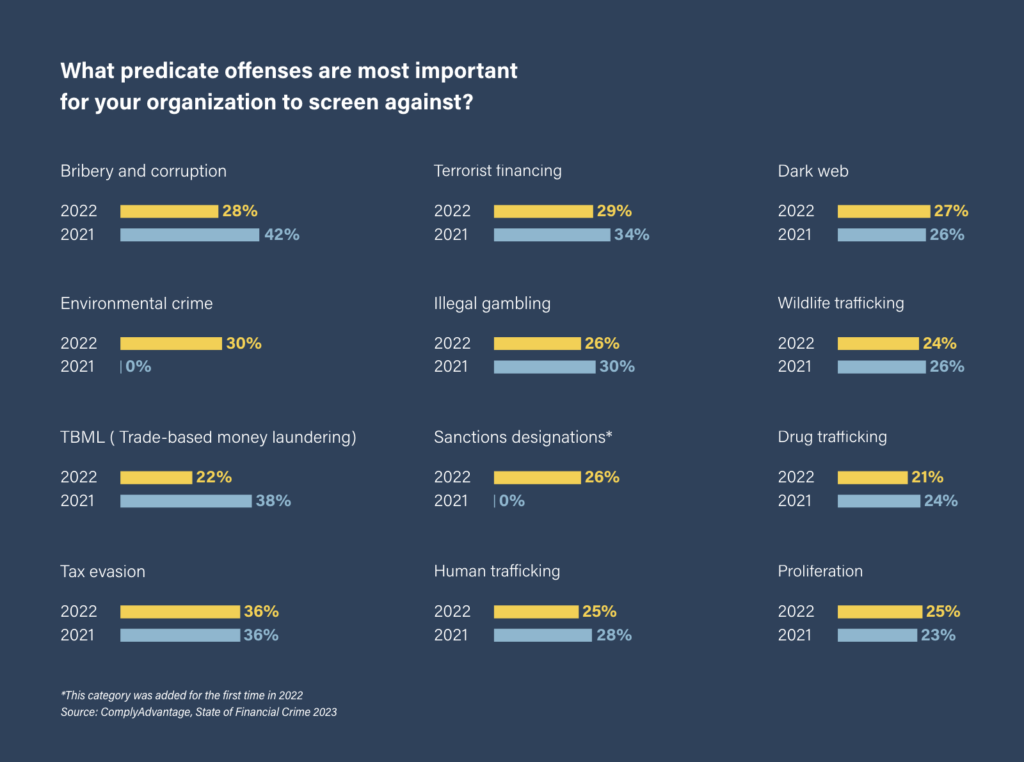

TBML takes advantage of the complex nature of trade systems, most prominently in international contexts where the involvement of multiple parties and jurisdictions make know your customer and anti-money laundering (KYC and AML) checks and customer due diligence (CDD) processes more difficult. In our State of Financial Crime Survey 2022, global compliance professionals rated TBML as the second most concerning criminal typology – behind only bribery and corruption. However, in our 2023 survey, TMBL dropped 16 points, with predicated crimes such as tax evasion, environmental crime, and terrorist financing taking the top spots. The high levels of concern around TBML in 2022 was largely due to COVID-related trade and supply chain issues, particularly in China. Since then, many firms have begun or are looking to embed supply chain risk management into their AML programs, with 45 percent of respondents saying they are focused on improving their management of supply chain risk in 2023 and beyond.

How does trade based money laundering work?

The most common TBML methods include:

Over-invoicing: The exporter submits an inflated invoice to the importer, generating a payment that exceeds the value of the shipped goods. Greater value is transferred from the importer to the exporter.

Under-invoicing: The exporter submits a deflated invoice to the importer, shipping goods with greater value and transferring that value to the importer.

Multiple-invoicing: The exporter invoices multiple times for the same shipment, transferring greater value from the importer to the exporter.

Over- or under-shipment: The exporter ships more goods than previously agreed with the importer, thereby transferring greater value to the importer. Alternatively, the exporter ships fewer goods than agreed, transferring greater value to the exporter.

Misrepresentation of quality: Goods shipped to importers are misrepresented on official documentation as being of a higher quality — thereby transferring greater value to the exporter.

Trade based money laundering examples

Practical examples of trade based money laundering activities that should raise red flags include:

A letter of credit for a high-value cross-border import is revealed to contain anomalies when examined by the routing bank. Further investigation by the bank reveals missing and unrecognized documentation with the import agents. The bank rejects the transaction and returns the drawing documents.

The first beneficiary of a multi-million dollar letter of credit is to supply medical goods for another country’s bureau of health. However, the second and ultimate beneficiary of the credit issues invoices that do not match those submitted by the first. The first beneficiary is revealed to have substituted invoices marked up by 300% and is additionally revealed to have a connection with the firm acting as the agent to the bureau of health. The bank cancels the transaction and adds the parties to their internal watch list.

Several shell companies purchase electronic goods with funds derived from criminal activities — and then sell the goods to buyers in high-risk countries with minimum due diligence. The proceeds are then directed back to the shell companies. The bank handling the transactions notices a number of red flags, in particular that the shell companies are registered in countries unrelated to the transactions. The bank adds all parties to its internal watch list.

TBML red flags

To combat trade based money laundering, firms should seek to strengthen their AML and KYC controls in trade finance and correspondent banking. Unfortunately, the complexity of those sectors means that many firms struggle to adjust their AML programs effectively. The fact that trade based money laundering is often hidden amongst legitimate trade activities, and stretched across different jurisdictions and organizations, adds to the challenge of detecting it.

Firms may find it easier to spot TBML activity if they are familiar with the methodologies associated with it. With that in mind, in 2021 the Financial Action Task Force (FATF) compiled a list of TBML risk indicators relevant to the public and private sectors. Those indicators include:

Structural risk indicators

Unusually complex or illogical corporate structures – such as the use of shell companies or companies in high-risk jurisdictions.

Trading entities registered at mass registration addresses with no reference to a specific unit – such as high-density residential or commercial buildings, or industrial complexes.

Trading entities with addresses that do not reflect the business in which they are engaged.

Trading entities that do not have an online presence or that have an online presence that does not reflect their stated business activities.

Trading entities with unexplained periods of dormancy.

Trading entities with names that mimic more-established competitors, and which may be attempts to appear affiliated with those competitors.

Trading risk indicators

Trading activity that does not reflect a stated line of business, for example, car dealers trading in textiles or precious metals.

Unusually complex trade deals such as deals that involve multiple third-party intermediaries, or that use needlessly complex trade routes.

Trading entities that overly complicate the use of financial products, intermingle different products or use a single product for an unusual amount of time.

Trading entities that consistently show unsustainably low profit margins or that make purchases clearly beyond their economic capabilities.

Newly-formed trading entities that engage in high-volume or high-value trades.

Document risk indicators

Inconsistencies or discrepancies across trade documents such as contracts and invoices.

Trade documents with values that are not consistent with market values or other comparable transactions.

Trade documents with only vague or very general references to the commodities being transported.

Missing, counterfeit, or falsified trade documents.

Trade documents that are unsuitably simple for the complexity of the deal they support.

Shipments that are routed through numerous jurisdictions with no economic or commercial justification.

Account and transaction risk indicators

Trading entities that make very late changes to payment arrangements.

Accounts engaging in high volumes of transactions that are inconsistent with their stated business activity.

Accounts that receive high volumes or deposits that are immediately transferred to other accounts, and that are left with a small end-of-day balance for no clear business reason.

Payments for imports made by parties other than the account holder.

Frequent cash deposits in amounts just under reporting thresholds.

How can we help with TBML?

Move away from delayed flat file uploads to configured automated monitoring. Screening against real-time data can help combat trade based money laundering.

While firms may learn to detect the key indicators of TBML, they face a range of compliance risks – not least the complexity of international trading systems and increasingly sophisticated criminal methodologies. Those challenges include:

Understanding pricing: In order to spot certain forms of TBML, firms must have a robust understanding of the reasonableness of the prices quoted in trades. The complexity of pricing systems, especially across international borders, can make the detection of TBML much more challenging. Firms may seek to reference international pricing standards or establish their own ‘price check’ database to verify relevant prices.

Understanding goods: Firms must work to understand what kinds of goods are being transferred by a particular entity. It is also important to establish whether those goods are ‘dual use’ which means that they may be used for both civil and military applications – and may therefore pose a high sanctions compliance risk.

Licensing: It may be difficult for firms to know when an import or export license is required for a transaction. Firms should seek advice on the types of goods that require licenses within their jurisdiction (and in foreign jurisdictions) to better manage the AML risk.

Document verification: Criminals may seek to duplicate or fake the documentation they submit as part of their trading activity. Accordingly, firms must seek to verify trade documentation wherever possible, including checking with issuing banks and requesting original copies.

Circumvention: Despite best efforts to confirm trade documents and other aspects of a transaction, money launderers may still find ways to circumvent AML checks in foreign jurisdictions. Where possible, firms should seek to confirm the delivery of goods to their expected destination.

Paper transactions: AML fortrade finance is often paper-based which can be a significant challenge for the efficiency of digital compliance controls. With that in mind, firms should seek to digitize trade documents wherever possible and take advantage of technological advancements to fully automate trade transactions.

TBML information sharing

To overcome the difficulties and challenges that TBML presents, firms should look beyond their own AML provisions and seek coordination with other organizations, law enforcement agencies, and government authorities. More specifically, banks and financial institutions should, where possible, share their tax-based money laundering discoveries and analyses because:

Information sharing between institutions makes it easier to identify the global criminal infrastructure and address specific instances of trade based money laundering.

Law enforcement agencies are incentivized to join an information-sharing network if it is more likely they will be able to stop criminal activity.

Government authorities can use information-sharing networks to analyze TBML and better align regulatory focus.

International guidance on trade based money laundering

The broader the regulatory perspective on TBML, the more effectively individual firms can work to prevent it. International authorities, including the FATF, issue guidance and advice to help financial institutions detect and address tax based money laundering. Aimed at national authorities, the FATF Trade Based Money Laundering Best Practice guidance focuses on raising private-sector awareness of the need for trade finance AML regulationsand on educating banking supervisors on TBML vulnerabilities in their AML/CFT programs.

The FATF also provides banks and financial institutions with a list of trade finance AML red flags to consider when managing cross-border transactions. The FATF’s TBML red flags include:

Significant discrepancies between invoices and the description of goods on official documents.

Shipments much larger or smaller than the usual traffic of goods handled by a particular importer or exporter.

Shipments routed through a number of countries or multiple unconnected subsidiaries without good reason.

Payment methods inconsistent with the level of risk presented by the transaction.

Shipments of goods typically considered at high risk of involvement in money laundering.

Shipments of goods into or out of countries deemed to present a high risk of money laundering.

Shipments that are paid for in cash.

Shipments that are paid for by third parties with no obvious connection to the transaction.

How to prevent and detect TBML

Since TBML can involve multiple parties and jurisdictions, some schemes can be very challenging to detect. To mitigate the threat of TBML, compliance teams should complete business-wide risk assessments as required to determine their risk exposure. Firms should then review their AML solutions in light of this assessment, making sure their tools are effectively calibrated according to their predefined risk appetite. Solutions to help detect and prevent TBML include:

AI-powered transaction monitoring – Legacy transaction monitoring solutions that rely on manual processes cannot keep up with the scale and speed of TBML. These solutions often produce a high frequency of false positive alerts, creating a backlog that delays compliance teams’ ability to uncover real risk. AI-powered transaction monitoring tools can reduce false positives by 70%, allowing teams to better prioritize their time and focus on the greatest risks to their business. Adopting a risk-based approach to TBML is crucial, so firms should consider partnering with a transaction monitoring provider that allows custom rule sets to be built and deployed quickly with the right thresholds set based on risk exposure.

Robust CDD – To uncover hidden relationships between exporters and importers, firms must implement CDD measures that are built on a combination of technology and expertise. To obtain a clear picture of who an entity is, their account’s ownership structures, and where they sit in the broader supply chain, compliance teams should ensure they have access to a real-time risk database of people and companies.

Reputable adverse media screening – Since adverse media can be a TBML structural risk indicator, firms should ensure their negative news screening solution can analyze true adverse media context at scale so no relevant information is missed. It’s also important that firms consider the frequency at which their adverse media solution updates. Best practice dictates that firms should have autonomous systems in place that refresh entity profiles within minutes of a change, lest a customer becomes subject to sanctions or negative news.

Demo Request

See how 1000+ leading companies are screening against the world's only real-time risk database of people and businesses

Disclaimer: This is for general information only. The information presented does not constitute legal advice. ComplyAdvantage accepts no responsibility for any information contained herein and disclaims and excludes any liability in respect of the contents or for action taken based on this information.

EN

EN FR

FR